WITH the new currency, Zimbabwe Gold (ZiG), hitting the market from tomorrow, the Reserve Bank of Zimbabwe (RBZ) has resorted to command economic measures — including Gestapo tactics — in a desperate bid to defend the shaky local unit buffeted by weak macro-economic fundamentals and lack of confidence.

BERNARD MPOFU

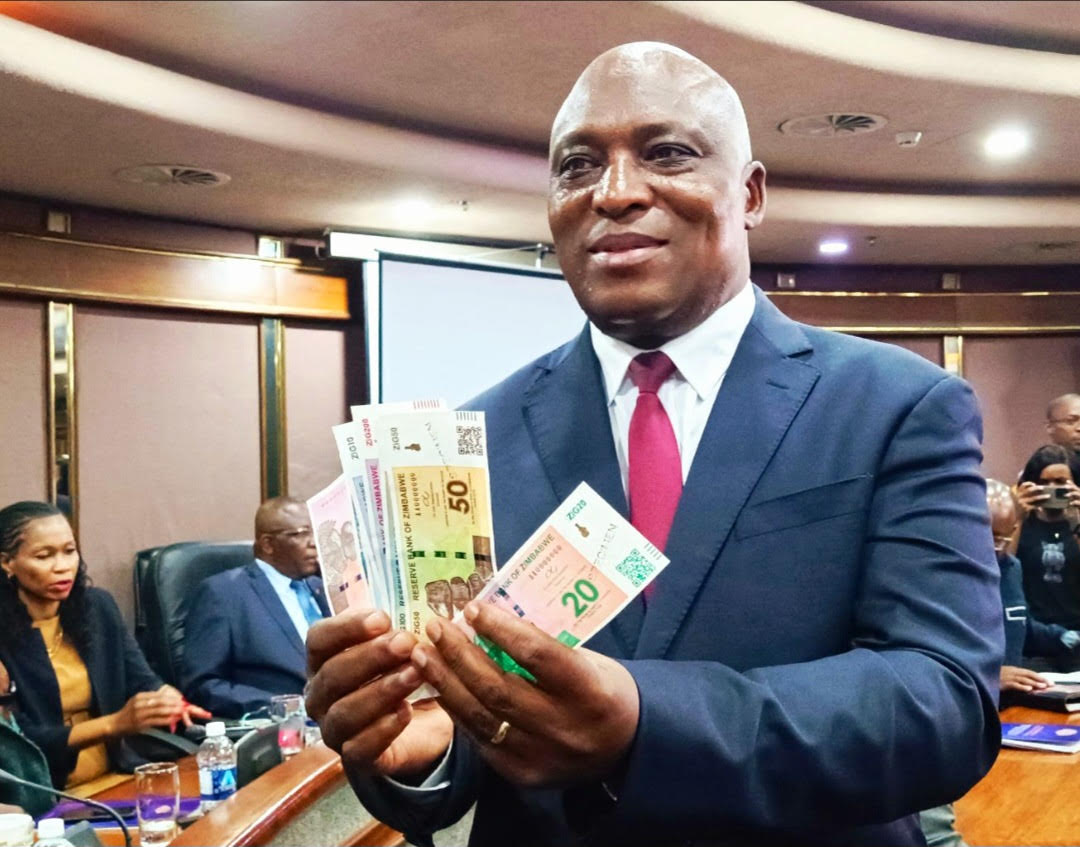

From tomorrow, banks will start receiving the new currency — ZiG1 to ZiG200 — while the public will begin to access the money on Tuesday.

However, RBZ governor John Mushayavanhu and his team have resorted to rigid controls to protect the weak currency, which has been greeted with suspicion, scepticism and derision.

While the authorities claim ZiG is backed by US$100m in foreign exchange reserves and 2.5 tonnes of gold valued at US$185 million, they have been running around in panicky mode to defend the currency which is fast-losing ground to base currencies, especially the United States dollar that overwhelmingly dominates the market.

Some of the rigid controls they have imposed in the market include a practically fixed exchange rate, aggressive mopping up of liquidity through market instruments, low bank withdrawal limits and virtual price controls.

The authorities are also using law and order instruments to deal with market forces in a bid to suppress the parallel market and control economic agents.

Gestapo tactics, including sweeping arrests, are being used to defend ZiG already struggling in the market as shown by the widening exchange rate differentials and arbitrage gap.

While the official exchange rate is US$1: ZiG13.56, in the market the rate has moved to at least US$1: ZiG20.

Parallel market traders see an opportunity, hence the RBZ’s tight liquidity control and arrests.

The authorities have descended onto the market with a heavy-handed crackdown: threats, arrests and prosecutions.

Vice-President Constantino Chiwenga a few days ago warned parallel market dealers that they would surely not want to see themselves crippled due to their activities.

“We wouldn’t want you to end up being crippled after being attacked,” Chiwenga threatened.

More than 70 black market forex dealers have been arrested of late in the police clampdown.

Finance permanent secretary George Guvamatanga has said Zimbabwe’s Treasury classifies illegal forex dealings as money laundering.

As part of the gamut of control measures, the RBZ has ordered banks to surrender their excess cash or liquidity, which is seizure of bank deposits.

Banks will now get Non-negotiable Certificates of Deposit yielding no interest.

Banks are to subsequently beg RBZ to meet their obligations by producing lists of individuals and companies who want their money before cash could be released to them.

The same applies to withdrawal limits. If banks and their clients want more than the miserably low withdrawal limits imposed, they have to beg and justify that first.

The RBZ holds the discretion, creating room for bottlenecks, rent-seeking and corruption.

This is part of authoritarian measures to mop up liquidity to control the exchange rate and inflation in an economy that has long plateaued and stabilised in crisis for decades.

It remains stuck in the doldrums despite optimistic official pronouncements, statistics and promises of growth and recovery.

The control measures amount to expropriation of liquidity, which throttles and distorts the market.

The RBZ’s Financial Intelligence Unit (FIU) has been operating on the ground, patrolling shops and monitoring transactions, while checking the exchange rate, prices and black market activities.

This command economic model approach is contrary to Mushayavanhu’s promise to introduce “a market-determined foreign exchange management system which links the local currency to a composite basket of reserve assets comprised of precious minerals (mainly gold) and foreign currency balances”.

In his recent monetary policy statement, Mushayavanhu diagnosed the disease, saying: “Currency and exchange rate instability has largely been driven by:

- High demand for foreign currency as a store of value.

- Reduced confidence due to continued currency volatility in recent months, and the widening margin between the interbank and parallel market exchange rates.

- Reduced use of the local currency for domestic transactions.

- Lack of certainty and predictability on the exchange rate front.”

To deal with the ailment, his prescription was: “In view of the above, the Reserve Bank will introduce a market-determined foreign exchange management system which links the local currency to a composite basket of reserve assets comprised of precious minerals (mainly gold) and foreign currency balances.”

Mushayavanhu also said he would ensure a stable currency; sustainable exchange rate; robust policy credibility; market confidence and solid macro-economic fundamentals.

However, on the ground he is not allowing “a market-determined exchange rate system” as he pledged.

The authorities are relying on crude measures to enforce exchange rate and pricing compliance.

The government has also been trying to pressure people to use ZiG in a market which is over 80% dominated by the United States dollar.

State enterprises, for instance Air Zimbabwe, are being forced to accept ZiG to give them a fair share of the market, yet the authorities fear allowing fuel, taxes and other obligations to be paid in local currency.

Mushayavanhu says increased demand for the local currency will “enhance its stability and role as a store of value and medium of exchange”.

But officials fear that if fuel is paid for in the uncertain and unstable ZiG, there may be shortages and the parallel market could explode.

They also fear if taxes are paid in ZiG, their budgets will be off the rails in an uncontrollable way, given the local currency’s poor store of value capacity.

When Mushayavanhu released his maiden monetary policy statement on 8 April as he also unveiled ZiG simultaneously, he made it appear as if he had a solid and viable plan.

However, his plan is unravelling — just three weeks into his new job.

This has left ZiG vulnerable, with some analysts pointing out the situation will not end well for the authorities and their psuedo-currency poorly clothed as a gold-backed means of exchange.

Analysts say while Mushayavanhu and his principals go around using Gestapo tactics, market forces cannot be arrested and their repressive measures will worsen or create market distortions.

Command measures: Command economic measures refer to government policies that dictate specific economic outcomes, often through direct control or regulation.

In the context of a fixed currency exchange rate and price controls, command interventions may include:

Fixed exchange rate: Government sets a fixed exchange rate between the local currency and a foreign currency.

Capital controls may be imposed to prevent currency fluctuations.

Price controls: Government sets maximum or minimum prices for goods and services, or alternatively use their agencies to police prices.

Price ceilings can limit profit margins, while price floors can guarantee a minimum income for producers.

This is not new. Zimbabwe has previously fixed the exchange rate and imposed price controls culminating in shortages of goods and forex, and the economic meltdown and hyperinflation crisis of 2008.

These measures are often implemented to address economic crises or stabilise prices, but they usually have unintended consequences.

Command economic measures, for instance, can lead to: Economic distortions; Shortages and scarcity; Black markets and corruption; Inefficient resource allocation; Reduced economic growth, innovation and prosperity.